Liquidation Protection Strategies 2025

Master proven strategies to protect your cryptocurrency loans from liquidation through monitoring, collateral management, and emergency response planning.

Introduction

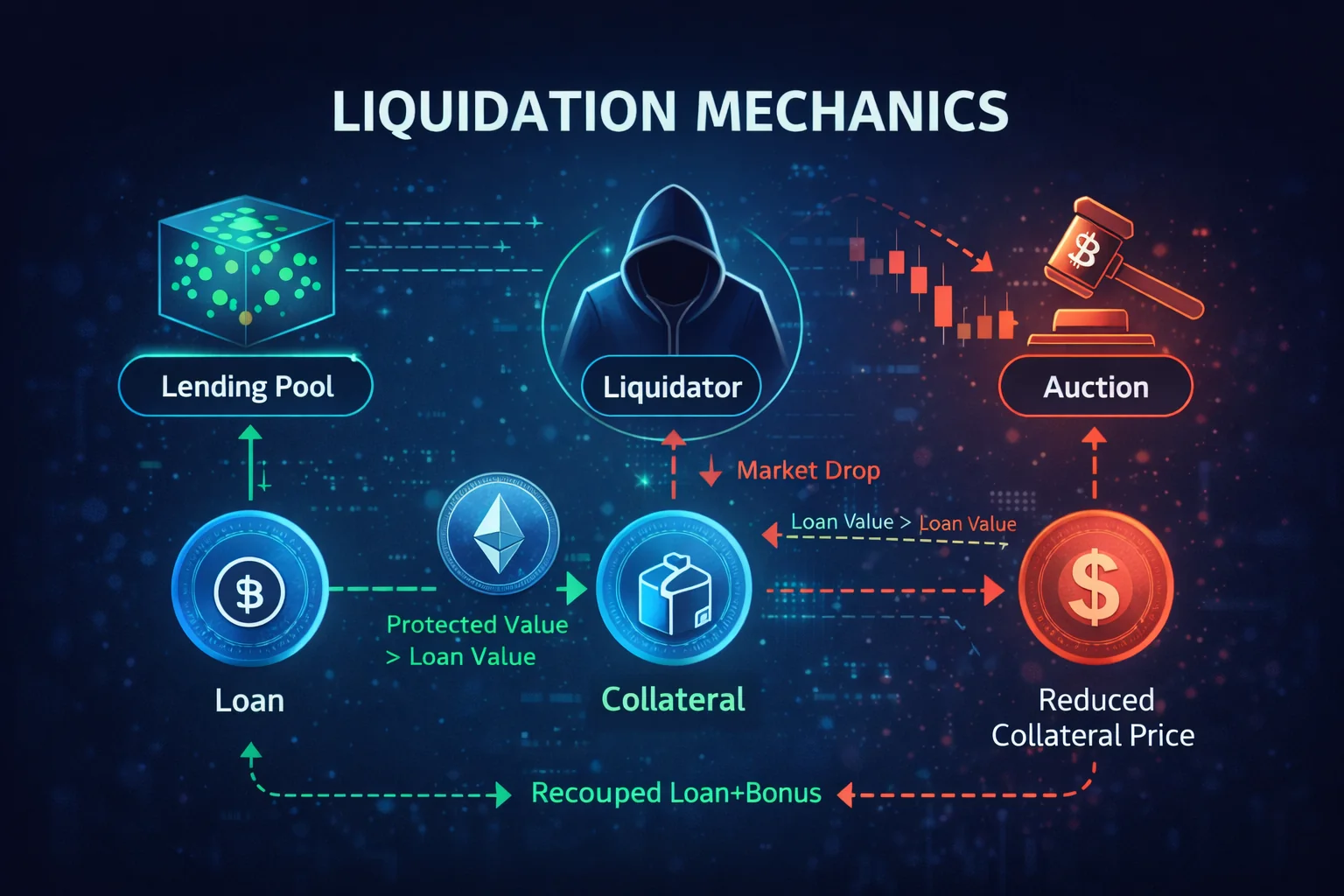

Liquidation protection represents one of the most critical skills for cryptocurrency lending participants. Digital assets are volatile. They can quickly transform profitable positions into devastating losses. Proper risk management is essential. Automated liquidation mechanisms execute without mercy. They trigger when loan-to-value ratios breach thresholds. This often results in collateral loss. Penalty fees can wipe out accumulated gains.

Understanding liquidation mechanics is fundamental. These systems operate differently from traditional finance. Human intervention isn't available. Smart contracts execute liquidations automatically. They use real-time price feeds. This happens during extreme market volatility. Prices can move dramatically within minutes. This automation provides efficiency and ensures transparency. But borrowers must implement sophisticated monitoring. They need response strategies.

The consequences of liquidation extend beyond immediate collateral loss. Borrowers face liquidation penalties. These typically range from 5% to 15%. Additional fees apply for gas costs. Protocol operations add more fees. In severe market downturns, cascading liquidations create feedback loops. Forced selling drives prices lower. This triggers additional liquidations. It creates systemic risks.

Successful liquidation protection requires a multi-layered approach. Combine conservative position sizing. Use active monitoring systems. Implement emergency response procedures. Deploy automated tools. These react faster than humans. Maintain significant safety margins. Diversify collateral across platforms. Use multiple asset types. Implement manual and automated systems. Add collateral when needed. Reduce debt when positions approach danger.

DeFi evolution has introduced new protection tools. These include automated position management services. Insurance protocols help. Sophisticated monitoring systems provide early warnings. They execute protective actions. However, these tools introduce new risks. They add complexities. Careful evaluation is required. Successful protection combines traditional risk management. It requires understanding cryptocurrency lending protocols.

This guide examines proven strategies for protecting cryptocurrency loans from liquidation. It covers basic monitoring techniques. It explains advanced automation systems. Whether you're conservative or advanced, understanding effective liquidation protection is essential for long-term success.

Market conditions in 2025 have highlighted the importance of robust liquidation protection. Several high-profile events serve as reminders. Leveraged cryptocurrency positions carry risks. Learning from these events helps. Implementing comprehensive protection measures prevents similar fates. You can still benefit from cryptocurrency lending opportunities.

The cryptocurrency lending landscape has matured significantly since its early days. Modern platforms offer sophisticated risk management tools. These include real-time health factor monitoring, automated collateral rebalancing, and predictive analytics that forecast liquidation risks before they materialise. Understanding how to leverage these tools effectively separates successful borrowers from those who experience devastating losses during market volatility.

Professional borrowers recognise that liquidation protection isn't merely about avoiding losses—it's about maintaining sustainable leverage that enables long-term wealth accumulation whilst managing downside risks. The strategies outlined in this comprehensive guide provide actionable frameworks for borrowers at all experience levels, from beginners taking their first crypto-backed loan to advanced users managing complex multi-protocol positions across various DeFi platforms.

Whether you're borrowing against Bitcoin on a centralised platform or managing a complex DeFi position across multiple protocols, the fundamental principles of liquidation protection remain consistent: maintain conservative collateral ratios, implement systematic monitoring, prepare emergency response procedures, and continuously adapt to changing market conditions. Mastering these principles transforms cryptocurrency lending from a risky speculation into a strategic financial tool that enhances portfolio performance whilst preserving capital through all market cycles.

Understanding Liquidation Mechanics

Liquidation mechanisms in cryptocurrency lending operate through sophisticated algorithms that continuously monitor collateral values against outstanding debt obligations, triggering automated asset sales when predetermined risk thresholds are breached. Understanding these mechanisms requires examining the mathematical formulas, oracle systems, and execution procedures that govern when and how liquidations occur across different lending platforms and protocols.

The fundamental principle underlying all liquidation systems is maintaining sufficient collateral coverage to protect lenders from default risk while providing borrowers with access to leverage. This balance is achieved through dynamic risk assessment models that account for asset volatility, market liquidity, and platform-specific risk parameters that determine safe borrowing limits and liquidation thresholds.

Health Factor Mathematical Framework

Health factor calculations on DeFi protocols like Aave involve complex mathematical relationships between collateral values, liquidation thresholds, and outstanding debt positions. The health factor formula: HF = (Sum of Collateral in ETH × Liquidation Threshold) / Total Borrows in ETH, provides a standardised risk metric that enables automated liquidation decisions across diverse asset portfolios.

Understanding health factor dynamics requires analysing how different collateral assets contribute to overall position safety based on their individual liquidation thresholds, which range from 50% for volatile altcoins to 95% for stablecoins. These thresholds reflect historical volatility patterns, market liquidity characteristics, and risk assessment models that determine appropriate safety margins for different asset classes.

- Above 3.0: Extremely safe position with substantial price buffer allowing for significant market volatility

- 2.0-3.0: Very safe position suitable for conservative borrowers with moderate risk tolerance

- 1.5-2.0: Safe position requiring regular monitoring during market volatility periods

- 1.2-1.5: Caution zone requiring daily monitoring and preparation for protective actions

- 1.0-1.2: Danger zone requiring immediate action to prevent liquidation within hours

- Below 1.0: Liquidation triggered automatically by protocol smart contracts

Advanced LTV Ratio Analysis for CeFi Platforms

Centralised lending platforms employ sophisticated risk management systems that calculate loan-to-value ratios using real-time market data, volatility assessments, and platform-specific risk models. These systems continuously monitor position health and implement graduated response procedures including margin calls, partial liquidations, and complete position closures based on predetermined risk parameters.

LTV calculations involve multiple variables, including current market prices, historical volatility metrics, liquidity assessments, and correlation analysis between different collateral assets. Advanced platforms implement dynamic LTV adjustments that respond to changing market conditions, increasing safety margins during periods of high volatility and relaxing requirements during stable market periods.

- Current LTV Formula: (Outstanding Loan Value / Current Collateral Value) × 100%

- Maximum LTV Limits: Platform-specific thresholds typically ranging from 50-90% depending on asset volatility

- Dynamic Adjustments: Real-time LTV modifications based on market volatility and liquidity conditions

- Margin Call Triggers: Warning thresholds typically set 10-20% below liquidation LTV

- Safe Operating Zone: Maintain current LTV 30-50% below maximum limits for optimal safety

Professional borrowers implement sophisticated LTV management strategies that account for correlation risks between collateral assets, interest rate fluctuations, and market volatility cycles. These strategies involve maintaining diversified collateral portfolios, implementing systematic rebalancing procedures, and utilising hedging instruments to manage directional market risk while preserving borrowing capacity.

Comprehensive Liquidation Trigger Analysis

Liquidation events result from complex interactions between market dynamics, technical systems, and protocol governance parameters that create cascading effects during periods of market stress. Understanding these trigger mechanisms enables borrowers to implement proactive protection strategies that account for both direct price movements and indirect factors that can precipitate liquidation events.

- Primary Price Movements: Direct collateral asset price declines that reduce position health factors

- Interest Rate Accumulation: Compound interest growth that increases debt obligations over time

- Oracle Price Feed Updates: Delayed or manipulated price feeds that trigger unexpected liquidations

- Network Congestion Effects: High gas fees and transaction delays that prevent protective actions

- Correlation Breakdown Events: Simultaneous declines in multiple collateral assets during market stress

- Liquidity Crisis Scenarios: Market conditions where asset sales cannot be executed at fair prices

- Governance Parameter Changes: Protocol updates that modify liquidation thresholds or risk parameters

- Technical System Failures: Smart contract bugs or oracle malfunctions that trigger erroneous liquidations

Advanced liquidation protection requires understanding these multifaceted trigger mechanisms and implementing comprehensive monitoring systems that track not only position health metrics but also broader market conditions, technical system status, and governance developments that could affect liquidation risk. Professional borrowers utilise sophisticated alert systems that monitor multiple risk factors simultaneously and provide early warning of potential liquidation scenarios.

Platform-Specific Liquidation Mechanisms and Risk Parameters

Different lending platforms implement unique liquidation mechanisms. Aave utilises a health factor system. It allows partial liquidations. Compound employs a collateral factor system. It has liquidation penalties of up to 50%. MakerDAO implements auction-based liquidations. Penalties vary based on market conditions.

Centralised platforms like Nexo and BlockFi offer more flexible procedures. They include margin calls. They provide grace periods. Customer service can intervene. This provides additional protection during volatility. However, these platforms carry counterparty risk. Regulatory uncertainty exists. Weigh these against forgiving liquidation procedures.

Professional borrowers often diversify across multiple platforms to reduce single-platform risk while accessing different liquidation mechanisms and risk parameters. This approach requires understanding the correlation risks between platforms, monitoring multiple positions simultaneously, and maintaining sufficient liquidity to respond to liquidation threats across different systems with varying response times and procedures.

Market Microstructure and Liquidation Cascades

Liquidation events can create cascading effects. They amplify market volatility. They trigger additional liquidations. During extreme stress, large liquidations overwhelm market liquidity. This causes price slippage. It triggers more liquidations. Understanding these effects is essential. Develop protection strategies that account for systemic risks.

Professional risk management includes monitoring market-wide liquidation risks. Use on-chain analytics. Track large position concentrations. Understand platform correlation. Advanced borrowers account for systemic risks. Maintain larger safety margins during stress. Avoid excessive leverage when risks are elevated.

DeFi protocols are interconnected. Liquidation events on one platform affect the entire ecosystem. Flash loan attacks can trigger unexpected liquidations. Oracle manipulations bypass traditional risk management. Stay informed about protocol developments whilst monitoring security incidents and governance proposals.

Monitoring Tools and Systems

Platform Native Dashboards

Aave Dashboard

- Health Factor: Real-time display with colour-coded risk indicators

- Liquidation Price: Calculated automatically with price alerts

- Borrow Limit: Shows available borrowing capacity and utilisation

- APY Tracking: Interest rate monitoring with historical trends

- Collateral Composition: Detailed breakdown of asset allocation

- Risk Parameters: Individual asset liquidation thresholds and LTV ratios

Nexo App

- LTV Ratio: Current and maximum displayed with visual indicators

- Collateral Value: Real-time USD value with 24-hour changes

- Loan Balance: Principal plus accrued interest breakdown

- Mobile Alerts: Push notifications for changes and thresholds

- Portfolio Analytics: Comprehensive performance tracking

- Risk Assessment: Automated risk scoring and recommendations

Third-Party Monitoring Tools

DeFi Saver (DeFi)

- Automation: Auto-repay or add collateral with custom triggers

- Alerts: Email/Telegram notifications with customizable thresholds

- Dashboard: Multi-protocol overview with unified interface

- Cost: Gas fees for automation plus 0.25% service fee

- Strategy Builder: Custom automation strategies with multiple conditions

- Historical Analysis: Performance tracking and optimisation suggestions

Instadapp (DeFi)

- Position Management: One-click adjustments across protocols

- Refinancing: Move between protocols for better rates

- Monitoring: Health factor tracking with predictive analytics

- Smart Accounts: Advanced wallet functionality with automation

- Yield optimisation: Automatic yield farming strategies

- Risk Management: Comprehensive risk assessment tools

Zerion (Multi-Platform)

- Portfolio Tracking: All DeFi positions with real-time updates

- Mobile App: iOS and Android with full functionality

- Alerts: Price and position notifications with custom triggers

- Transaction History: Comprehensive activity tracking

- Performance Analytics: Detailed profit/loss analysis

- Multi-Chain Support: Ethereum, Polygon, BSC, and more

Advanced Price Alert Systems

Multi-Level Alert System

Example for ETH collateral with 150% ratio:

- Level 1 (Warning): ETH drops 10% - monitor daily, review position

- Level 2 (Caution): ETH drops 15% - prepare action, check emergency funds

- Level 3 (Action): ETH drops 20% - add collateral or reduce debt

- Level 4 (Critical): ETH drops 25% - immediate response required

- Level 5 (Emergency): ETH drops 30% - maximum protective measures

Professional Alert Tools

- TradingView: Custom price alerts with technical analysis integration

- CoinGecko: Mobile app notifications with portfolio tracking

- Telegram Bots: Instant messaging alerts with custom commands

- Discord Bots: Community alert channels with shared monitoring

- Webhook Integration: Custom API alerts for advanced users

- SMS Alerts: Critical notifications via text message

Comprehensive Monitoring Infrastructure for Professional Borrowers

Professional cryptocurrency borrowers implement sophisticated monitoring infrastructure that combines multiple data sources, automated analysis systems, and comprehensive alert mechanisms to provide early warning of potential liquidation scenarios across diverse lending platforms and market conditions. This infrastructure includes real-time market data feeds, on-chain analytics, social sentiment monitoring, and macroeconomic indicators that could affect cryptocurrency prices and liquidation risk.

Advanced monitoring systems integrate with multiple lending platforms simultaneously, providing unified dashboards that display position health metrics, correlation analysis between different collateral assets, and predictive models that forecast liquidation risk based on historical volatility patterns and current market conditions. These systems enable professional borrowers to manage complex multi-platform portfolios while maintaining comprehensive oversight of liquidation risk across all positions.

Professional monitoring infrastructure includes automated stress testing capabilities that simulate various market scenarios and their potential impact on borrowing positions across different platforms and collateral types. These stress testing systems help borrowers understand their portfolio's resilience to various market conditions and identify potential vulnerabilities before they become critical threats to position stability.

Real-Time Risk Assessment and Predictive Analytics

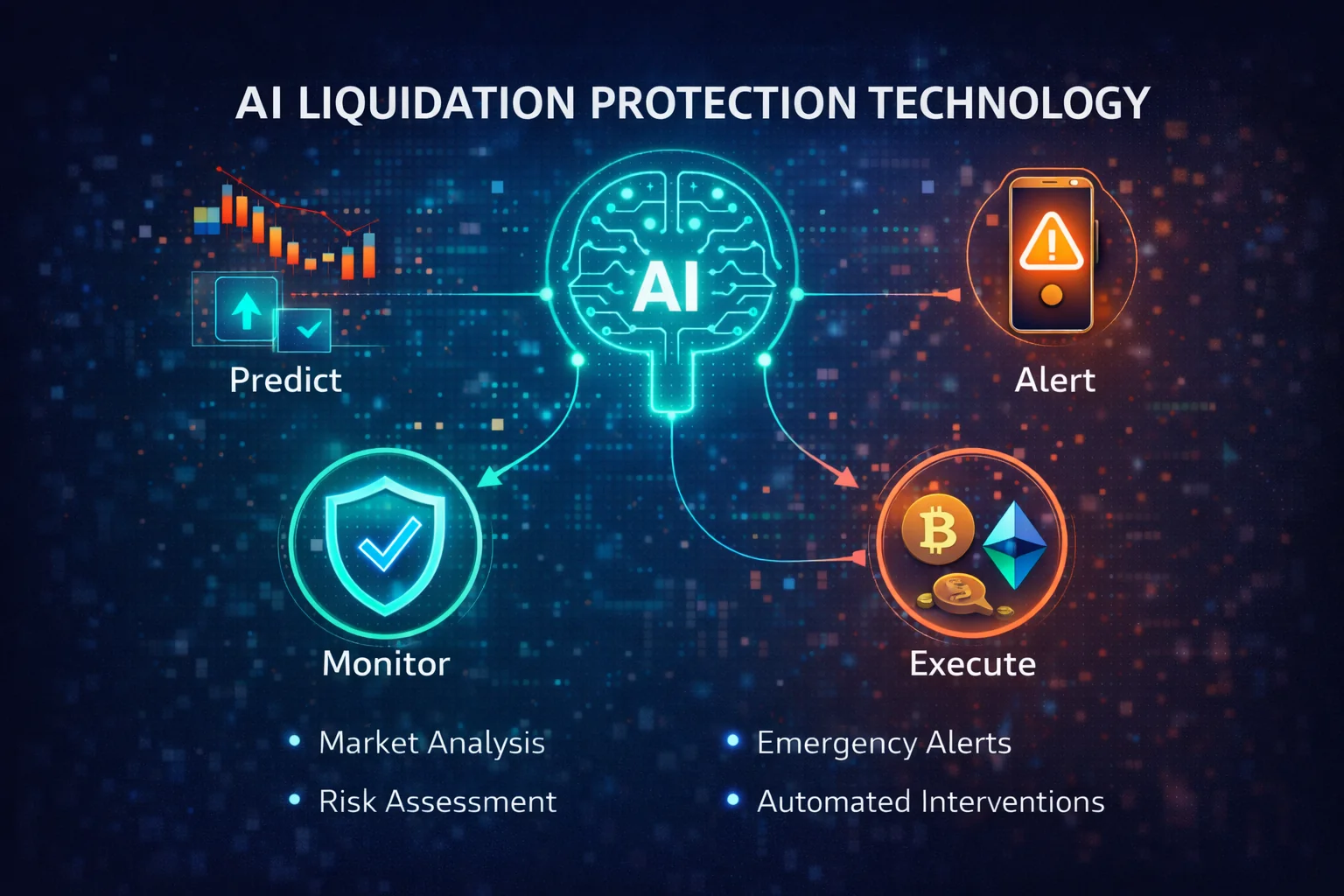

Modern liquidation protection systems utilise machine learning algorithms and predictive analytics to assess liquidation risk in real-time, incorporating multiple data sources including market volatility, correlation patterns, liquidity conditions, and historical liquidation events to provide sophisticated risk assessment and early warning capabilities. These systems can identify potential liquidation scenarios before traditional metrics indicate danger, enabling proactive protective measures.

Predictive analytics systems analyse patterns in market behavior, social sentiment, and on-chain activity to identify conditions that historically precede liquidation cascades or extreme volatility events. By understanding these patterns, borrowers can implement preemptive protective measures during periods of elevated risk, even when their individual positions appear healthy according to traditional metrics.

Advanced risk assessment includes correlation analysis between different collateral assets, lending platforms, and market conditions to identify systemic risks that could affect multiple positions simultaneously. This analysis helps borrowers understand the interconnected nature of their liquidation risk and implement appropriate diversification strategies to reduce correlation exposure.

Automated Response Systems and Emergency Procedures

Professional liquidation protection includes automated response systems that can execute protective actions faster than manual intervention allows, utilising smart contracts, API integrations, and automated trading systems to add collateral, reduce debt, or execute hedging strategies when predetermined risk thresholds are breached. These systems operate continuously, providing protection during periods when manual monitoring is impossible.

Emergency response procedures include comprehensive protocols for different types of liquidation threats, from gradual market declines to flash crashes and technical system failures. These procedures specify exact actions to take under different scenarios, including contact information for emergency support, backup systems for critical operations, and recovery procedures for various types of incidents.

Automated systems include fail-safe mechanisms and manual override capabilities to prevent erroneous actions while ensuring rapid response when genuine threats are detected. These systems require careful configuration and regular testing to ensure they operate correctly during actual emergency situations when quick action is essential for position protection.

Prevention Strategies

Strategy 1: Conservative LTV Ratios

Recommended Safe Ratios

- Bitcoin: 30-40% LTV (liquidation at 50-60%)

- Ethereum: 25-35% LTV (liquidation at 45-55%)

- Major Altcoins: 20-30% LTV (liquidation at 40-50%)

- Stablecoins: 70-80% LTV (liquidation at 85-95%)

Buffer Calculation

Example: Platform liquidates at 80% LTV

- Aggressive: Borrow at 70% LTV (12.5% buffer)

- Moderate: Borrow at 60% LTV (25% buffer)

- Conservative: Borrow at 50% LTV (37.5% buffer)

Strategy 2: Emergency Collateral Fund

Fund Size Calculation

Maintain liquid reserves equal to 20-30% of loan value:

- $10,000 loan: Keep $2,000-3,000 in stablecoins

- $50,000 loan: Keep $10,000-15,000 ready

- $100,000 loan: Keep $20,000-30,000 accessible

Fund Storage

- Hot Wallet: Instant access for emergencies

- Stablecoins: USDC, USDT, DAI for stability

- Same Chain: Match your loan platform's blockchain

- Gas Reserves: Keep ETH/native tokens for transactions

Strategy 3: Diversified Collateral

Multi-Asset Approach

Spread collateral across assets with different volatility profiles:

- 50% Bitcoin: Lower volatility, stable base

- 30% Ethereum: Moderate volatility

- 20% Stablecoins: Zero volatility buffer

Benefits

- Reduces single-asset risk

- Balances volatility exposure

- Provides internal rebalancing options

Strategy 4: Partial Loan Repayment

Scheduled Repayments

- Monthly: Repay 5-10% of principal

- Quarterly: Larger 15-20% repayments

- Profit-Based: Repay when investments profit

Benefits

- Gradually improves HF

- Reduces interest costs

- Builds safety buffer over time

- Psychological comfort

Emergency Response Procedures

Action Plan by Health Factor

Health Factor 1.5-2.0 (Caution)

- Action: Monitor daily instead of weekly

- Prepare: Have emergency funds ready

- Consider: Small collateral addition (5-10%)

- Timeline: No immediate urgency

Health Factor 1.2-1.5 (Warning)

- Action: Add 10-20% more collateral

- Alternative: Repay 10-15% of loan

- Monitor: Check multiple times daily

- Timeline: Act within 24-48 hours

Health Factor 1.0-1.2 (Critical)

- Immediate Action: Add 30%+ collateral NOW

- Or: Repay 25%+ of loan immediately

- Monitor: Continuously until safe

- Timeline: Act within hours

Health Factor Below 1.0 (Liquidation)

- Too Late: Liquidation already triggered or imminent

- Last Chance: Massive collateral addition (50%+)

- Reality: Usually too late to prevent

- Learn: analyse what went wrong

Emergency Response Options

Option 1: Add Collateral

Best when: You have emergency funds ready

- Pros: Keeps loan active, maintains position

- Cons: Requires liquid capital

- Speed: 5-15 minutes (DeFi), instant (CeFi)

Option 2: Partial Repayment

Best when: You want to reduce exposure

- Pros: Reduces debt, improves ratio

- Cons: Uses borrowed capital

- Speed: 5-15 minutes (DeFi), instant (CeFi)

Option 3: Close Position

Best when: Market outlook very negative

- Pros: Eliminates liquidation risk

- Cons: Loses position, pays full interest

- Speed: 10-20 minutes

Option 4: Collateral Swap

Best when: One asset dropping, another stable

- Pros: Rebalances without adding capital

- Cons: Complex, gas fees, slippage

- Speed: 15-30 minutes

Market Crash Response

During Flash Crash

- Don't Panic: Assess situation calmly

- Check Health: Current HF/LTV

- Network Status: Gas fees and congestion

- Act Fast: If critical, act immediately

Network Congestion Strategy

- High Gas: Pay premium for fast confirmation

- Alternative Chains: Use L2 or other chains if available

- Batch Transactions: Combine actions to save gas

Automation and Advanced Tools

DeFi Automation Platforms

DeFi Saver Automation

Features:

- Auto-Repay: Automatically repay when HF drops

- Auto-Boost: Automatically borrow more when safe

- Custom Triggers: Set your own thresholds

- Cost: 0.25% fee + gas costs

Setup Example:

- Trigger: Health factor drops below 1.8

- Action: Repay 10% of the loan

- Source: Use collateral or external wallet

Instadapp Automation

- Smart Wallet: Automated position management

- Refinancing: Auto-move to better rates

- Rebalancing: Maintain target HF

Custom Alert Systems

Telegram Bot Setup

Create custom alerts using Telegram bots:

- Price Alerts: Collateral asset price drops

- Health Alerts: Health factor changes

- Gas Alerts: Network congestion warnings

Webhook Integration

For advanced users:

- Connect wallet to monitoring service

- Set up webhooks for position changes

- Receive instant notifications

- Integrate with trading bots if needed

Pros and Cons of Automation

Advantages

- 24/7 monitoring without manual effort

- Instant response to market changes

- Removes emotional decision-making

- Can act during sleep or travel

Disadvantages

- Smart contract risk (automation bugs)

- Gas costs for automated transactions

- May trigger unnecessarily in volatility

- Requires technical setup

Advanced Protection Strategies for 2025

Multi-Chain liquidation safety

Advanced users deploy liquidation safety across multiple blockchain networks. This reduces single-chain risks. It optimises gas costs. Maintain collateral on different chains. Keep emergency funds ready. Use cross-chain bridges for rapid asset movement. This works during market stress.

Popular setups include Ethereum mainnet for large positions. Use Polygon for cost-effective monitoring. Choose Arbitrum for medium-sized positions. These offer lower gas costs. Cross-chain protocols like LayerZero enable automated protection. Chainlink CCIP helps too. But understand bridge risks. Know timing delays.

Algorithmic margin safety

Sophisticated investors use algorithmic protection systems. These automatically adjust positions. They respond to market conditions. They analyse volatility metrics. They study correlation patterns. Systems can add collateral automatically. They can partially close positions. They can hedge exposure using derivatives. This happens when liquidation risk increases.

Popular solutions include DeFiSaver's automation. Try Instadapp's position management. Consider custom smart contracts. These execute predefined protection strategies. They require careful configuration. They need regular monitoring. But they provide 24/7 protection. No manual intervention needed.

Insurance and Protection Protocols

Emerging insurance protocols offer collateral protection coverage. Nexus Mutual provides this. InsurAce offers coverage too. Other decentralised platforms help. They cover smart contract failures. They protect against oracle malfunctions. They handle technical risks. These could lead to unfair liquidations.

Insurance doesn't prevent market-driven liquidations. But it protects against technical failures. It compensates for protocol bugs. It covers oracle manipulation. Consider insurance costs carefully. Include them in your borrowing strategy. This matters especially for large positions.

Platform-Specific Liquidation Considerations

Aave Liquidation Mechanics

Aave uses a health factor system where positions become eligible for liquidation when the health factor drops below 1.0. The platform offers partial liquidations, meaning only a portion of your collateral is liquidated to restore the health factor above 1.0. Aave also provides liquidation safety through its Safety Module and governance-backed insurance fund.

Key Aave features for position protection include isolation mode for new assets, efficiency mode (eMode) for correlated assets, and supply/borrow caps that limit systemic risk. Understanding these features helps optimise your borrowing strategy and minimise liquidation risk on the platform.

Compound Liquidation System

Compound uses a collateral factor system where each asset has a specific collateral factor determining how much you can borrow against it. Liquidations occur when your account liquidity becomes negative, and liquidators can purchase up to 50% of your debt at a discount.

Compound's governance token (COMP) holders can vote on risk parameters, collateral factors, and liquidation incentives. Staying informed about governance proposals helps anticipate changes that might affect your positions and liquidation risk.

MakerDAO Vault Management

MakerDAO vaults (formerly CDPs) have specific liquidation ratios for different collateral types. The platform uses a liquidation auction system where collateral is sold to cover debt plus penalties. MakerDAO offers various vault types with different risk parameters and liquidation ratios.

Advanced MakerDAO users can utilise vault automation services like DeFiSaver, Instadapp, or B.Protocol to automatically manage their positions and prevent liquidations. These services can automatically add collateral, pay down debt, or execute more complex strategies based on predefined parameters.

centralised Platform Considerations

centralised platforms like Nexo, BlockFi, and Celsius (before its collapse) have different liquidation procedures compared to DeFi protocols. These platforms typically offer more flexible liquidation safety, including margin calls, grace periods, and customer service intervention.

However, centralised platforms also carry counterparty risk, regulatory risk, and potential for platform-wide issues affecting all users simultaneously. The collapse of several major centralised lending platforms in 2022 highlighted the importance of understanding these additional risks when choosing position protection strategies.

Regulatory and Tax Implications of margin safety

Tax Treatment of Liquidations

Liquidation events can have significant tax implications depending on your jurisdiction. In many countries, liquidations are treated as taxable disposals of assets, potentially triggering capital gains or losses. Understanding these implications helps in planning collateral protection strategies that minimise tax burdens.

Some jurisdictions treat liquidations differently from voluntary sales, while others may allow loss harvesting opportunities when liquidations result in losses. Consult with tax professionals familiar with cryptocurrency regulations in your jurisdiction to understand the specific implications for your situation.

Regulatory Compliance Considerations

Different jurisdictions have varying regulations regarding cryptocurrency borrowing and lending activities. Some regions require specific licenses for lending platforms, while others have restrictions on certain types of DeFi activities. Understanding these regulations helps ensure your liquidation protection strategies remain compliant with local legal requirements.

Regulatory changes can also affect platform availability, interest rates, and liquidation procedures. Stay informed about regulatory developments in your jurisdiction and consider how they might impact your borrowing and liquidation protection strategies for optimal risk management practices and long-term success.

Advanced Liquidation Protection Strategies and Professional Techniques

Multi-Platform Risk Distribution and Portfolio Management

Advanced liquidation protection requires sophisticated portfolio management techniques that distribute risk across multiple platforms, collateral types, and market conditions to minimise exposure to single points of failure. Professional cryptocurrency borrowers implement comprehensive risk distribution strategies that include platform diversification, collateral asset diversification, and temporal diversification of borrowing activities to reduce correlation risks and systematic vulnerabilities that could trigger simultaneous liquidations across multiple positions.

Multi-platform strategies involve maintaining borrowing positions across different lending protocols, each with distinct liquidation parameters, oracle systems, and risk management approaches. This diversification protects against platform-specific risks including smart contract vulnerabilities, oracle failures, governance attacks, and operational disruptions that could affect liquidation thresholds or trigger unexpected liquidation events. Professional borrowers typically maintain detailed spreadsheets tracking positions across platforms, monitoring aggregate exposure, and ensuring no single platform represents more than 30-40% of total borrowing exposure.

Dynamic Hedging Strategies and Market Neutral Positions

Sophisticated borrowers employ dynamic hedging strategies that maintain market-neutral or delta-neutral positions to protect against adverse price movements while preserving access to borrowed capital. These strategies involve using derivatives, perpetual futures, and options to hedge collateral exposure, effectively decoupling liquidation risk from market direction while maintaining the ability to benefit from specific investment opportunities or arbitrage situations that require leveraged capital.

Market-neutral hedging requires continuous monitoring and adjustment as market conditions change, with professional traders using automated systems to maintain hedge ratios and rebalance positions based on volatility, correlation changes, and time decay factors. These sophisticated approaches enable borrowers to maintain higher loan-to-value ratios safely by eliminating directional market risk, though they require advanced understanding of derivatives markets and sophisticated execution capabilities.

Automated Risk Management Systems and Algorithmic Protection

Professional cryptocurrency borrowers increasingly rely on automated risk management systems that monitor positions continuously, execute protective actions based on predefined parameters, and respond to market conditions faster than manual intervention allows. These systems integrate with multiple lending platforms, exchange APIs, and market data feeds to provide comprehensive position monitoring, automated rebalancing, and emergency liquidation protection across complex multi-platform portfolios.

Algorithmic protection systems can execute sophisticated strategies including automated collateral additions, partial position closures, hedge adjustments, and emergency liquidations based on market volatility, correlation changes, and platform-specific risk factors. These systems operate continuously, providing protection during periods when manual monitoring is impossible, and can respond to market events within seconds rather than minutes or hours required for manual intervention.

Insurance and Protection Protocols Integration

Emerging insurance protocols and protection mechanisms provide additional layers of liquidation protection through smart contract-based coverage, mutual insurance pools, and parametric insurance products that compensate borrowers for liquidation events under specific circumstances. These protocols represent innovative approaches to socializing liquidation risk and providing compensation for borrowers who experience liquidations due to platform failures, oracle manipulations, or extreme market events beyond normal volatility parameters.

Integration with protection protocols requires understanding coverage terms, premium costs, and claim procedures, with professional borrowers evaluating insurance costs against potential liquidation losses to determine optimal coverage levels. These emerging solutions complement traditional risk management approaches and provide additional safety nets for sophisticated borrowing strategies, though they require careful evaluation of counterparty risks and coverage limitations.

Stress Testing and Scenario Analysis Frameworks

Professional liquidation protection involves comprehensive stress testing and scenario analysis that evaluates portfolio resilience under various market conditions, including historical volatility events, correlation breakdowns, and extreme market scenarios that could trigger liquidation cascades. These analytical frameworks help borrowers understand potential vulnerabilities, optimise position sizing, and develop contingency plans for various market scenarios that could threaten position stability.

Stress testing methodologies include Monte Carlo simulations, historical backtesting, and scenario analysis based on extreme market events from traditional and cryptocurrency markets. Professional borrowers use these analytical tools to optimise their liquidation protection strategies, determine appropriate safety margins, and develop response procedures for various market scenarios that could threaten their positions across multiple platforms and collateral types.

Regulatory Compliance and Institutional Standards

Institutional cryptocurrency borrowers must navigate complex regulatory environments whilstimplementing liquidation protection strategies that comply with applicable financial regulations, reporting requirements, and risk management standards. Professional operations implement comprehensive compliance frameworks that document risk management procedures, maintain detailed audit trails, and ensure liquidation protection strategies align with institutional risk management policies and regulatory expectations.

Compliance considerations include position reporting requirements, risk disclosure obligations, and adherence to institutional investment guidelines that may restrict leverage levels, platform usage, or collateral types. Professional borrowers work with legal and compliance teams to ensure their liquidation protection strategies meet regulatory requirements whilstmaximising capital efficiency and investment opportunities within approved risk parameters and operational constraints.

Advanced Liquidation Protection for Professional Borrowers

Institutional Risk Management Frameworks

Professional cryptocurrency borrowing operations require sophisticated risk management frameworks that integrate quantitative risk models, stress testing, and comprehensive monitoring systems to prevent liquidation events across complex multi-platform portfolios. Institutional-grade liquidation protection includes automated rebalancing systems, sophisticated hedging strategies, and comprehensive risk monitoring that enables proactive position management and systematic liquidation prevention through professional risk management techniques.

Advanced institutional strategies encompass portfolio-level risk management, cross-platform position coordination, and sophisticated derivatives strategies that provide comprehensive liquidation protection while maintaining optimal capital efficiency and borrowing capacity. Professional implementation requires substantial investment in risk management infrastructure, ongoing operational costs, and comprehensive compliance frameworks that ensure effective liquidation protection while maintaining regulatory compliance and operational efficiency.

Quantitative Risk modelling and Predictive Analytics

Professional liquidation protection utilises sophisticated quantitative models that predict liquidation risks based on market volatility, correlation analysis, and systematic risk factors that enable proactive position management and strategic risk mitigation. Advanced modelling techniques include Monte Carlo simulations, stress testing, and comprehensive scenario analysis that provide detailed insights into liquidation risks under different market conditions and enable strategic position adjustments to maintain optimal risk profiles.

Predictive analytics systems integrate real-time market data, historical volatility patterns, and systematic risk factors to provide early warning systems that enable proactive liquidation protection through strategic position adjustments and risk mitigation strategies. Professional implementation includes automated alerting systems, systematic monitoring procedures, and comprehensive reporting frameworks that enable effective risk management and liquidation prevention through data-driven decision-making and strategic position management designed for optimal risk-adjusted returns and comprehensive liquidation protection.

Psychological Aspects of Liquidation Protection and Behavioural Risk Management

Cognitive Biases and Decision-Making Under Pressure

Liquidation protection success depends not only on technical systems and risk management procedures but also on understanding and managing the psychological factors that influence decision-making during periods of market stress and volatility. Cognitive biases including loss aversion, anchoring bias, and overconfidence can lead to poor decisions that increase liquidation risk, while emotional responses like fear and greed can cause borrowers to abandon systematic protection strategies at critical moments when disciplined execution is most important.

Professional risk managers recognise that psychological factors often override rational decision-making during market crises, leading to behaviours that increase rather than decrease liquidation risk. Common psychological pitfalls include refusing to add collateral due to loss aversion, waiting too long to take protective action due to anchoring on previous price levels, and making impulsive decisions based on short-term market movements rather than systematic risk assessment procedures.

Effective liquidation protection strategies incorporate behavioural risk management techniques that account for psychological factors and implement systematic procedures that reduce reliance on emotional decision-making during critical moments. These approaches include pre-committed action plans, automated systems that remove emotional decision-making from critical moments, and systematic procedures that provide clear guidance for different scenarios without requiring complex real-time analysis under pressure.

Systematic Approach to Stress Management and Decision Protocols

Developing systematic approaches to liquidation protection requires creating comprehensive decision-making frameworks that provide clear guidance for different market scenarios while accounting for the psychological pressures that affect judgement during periods of high volatility and market stress. Professional borrowers implement detailed protocols that specify exact actions to take under different conditions, removing the need for complex decision-making during emotionally charged situations.

Effective stress management protocols include regular practice of emergency procedures, systematic review of protection strategies during calm market periods, and development of muscle memory for critical actions that can be executed automatically during high-stress situations. These approaches help borrowers maintain disciplined execution of protection strategies even when market conditions create psychological pressure to deviate from systematic procedures.

Professional decision protocols incorporate multiple checkpoints and verification procedures that prevent impulsive actions while ensuring rapid response when protective measures are needed. These systems include mandatory cooling-off periods for major decisions, requirement for multiple confirmations before executing significant changes, and systematic procedures for evaluating the effectiveness of protection strategies and making necessary adjustments based on performance analysis rather than emotional reactions.

Long-term Perspective and Sustainable Risk Management Practices

Successful liquidation protection requires maintaining a long-term perspective that prioritises sustainable risk management practices over short-term yield optimisation or speculative positioning that increases liquidation risk. Professional borrowers understand that liquidation protection is an ongoing process that requires continuous attention, regular strategy updates, and systematic improvement based on market evolution and personal experience with different protection techniques.

Sustainable risk management practices include regular review and updating of protection strategies, systematic analysis of near-miss events and successful protection implementations, and continuous education about new tools and techniques that can enhance liquidation protection effectiveness. These approaches help borrowers adapt their strategies to changing market conditions while maintaining the disciplined approach necessary for long-term success in cryptocurrency lending and borrowing activities.

The psychological aspects of liquidation protection extend beyond individual decision-making to include understanding market psychology and crowd behaviour that can create systemic risks during periods of widespread liquidation events. Professional risk managers monitor market sentiment indicators, social media trends, and behavioral signals that may indicate increased liquidation risk across the broader market, enabling proactive adjustments to protection strategies before widespread liquidation events create additional market stress and volatility.

Effective liquidation protection is the cornerstone of successful cryptocurrency lending and borrowing, requiring a comprehensive approach that combines conservative position sizing, active monitoring, and robust emergency response procedures. The volatile nature of cryptocurrency markets makes liquidation protection not just advisable but essential for anyone seeking to use leverage or access liquidity through collateralized loans.

The strategies outlined in this guide provide multiple layers of protection against liquidation, from basic monitoring and alert systems to sophisticated automated tools and emergency response procedures. The key to success lies in implementing multiple complementary strategies rather than relying on any single approach, as market conditions can change rapidly and unexpectedly in the cryptocurrency space.

Conservative position sizing remains the most effective protection strategy, with experienced borrowers typically maintaining loan-to-value ratios well below platform maximums to provide substantial safety margins. Combined with active monitoring, diversified collateral, and emergency funds, conservative positioning can protect against all but the most extreme market events while still providing access to the benefits of cryptocurrency lending.

As the DeFi ecosystem continues to evolve, new tools and strategies for liquidation protection are constantly emerging, from automated position management services to insurance protocols and sophisticated risk management platforms. However, these innovations should complement, not replace, fundamental risk management principles and personal responsibility for monitoring and protecting positions.

The future of cryptocurrency lending will likely bring improved user interfaces, better risk management tools, and more sophisticated protection mechanisms, but the fundamental principles of liquidation protection will remain constant. Success requires discipline, preparation, and a thorough understanding of the risks involved in cryptocurrency lending and borrowing activities.

By implementing the strategies and best practices outlined in this guide, borrowers can significantly reduce their liquidation risk while still accessing the benefits of cryptocurrency lending. Remember that liquidation protection is an ongoing process that requires constant attention and adjustment as market conditions change, but the effort invested in proper risk management will pay dividends in protecting your capital and achieving long-term success in cryptocurrency lending.

Institutional Liquidation Protection Frameworks and Professional Risk Management

Quantitative Risk Assessment Models for Liquidation Prevention

Professional cryptocurrency lending operations employ sophisticated quantitative risk assessment models that integrate multiple data sources, including real-time market volatility metrics, correlation analysis between different collateral assets, liquidity depth assessments, and macroeconomic indicators that influence cryptocurrency market dynamics. These models utilise advanced statistical techniques including Monte Carlo simulations, Value-at-Risk calculations, and stress testing scenarios that evaluate portfolio resilience under various market conditions and extreme volatility events.

Institutional risk management frameworks incorporate machine learning algorithms that analyse historical liquidation events, market microstructure data, and behavioural patterns to identify early warning signals that precede liquidation cascades. These systems continuously update risk parameters based on changing market conditions, implementing dynamic position sizing algorithms that automatically adjust exposure levels based on volatility forecasts, correlation breakdowns, and liquidity constraints that could affect liquidation execution during market stress periods.

Advanced quantitative models account for second-order effects, including correlation breakdown during market stress, liquidity evaporation in volatile conditions, and the impact of large liquidation events on market prices. Professional risk managers implement sophisticated hedging strategies that utilise derivatives, cross-asset arbitrage, and systematic rebalancing procedures to maintain optimal risk-adjusted returns while minimising liquidation probability across diverse market scenarios and volatility regimes.

Multi-Platform Risk Distribution and Portfolio optimisation

Institutional liquidation protection strategies involve sophisticated portfolio optimisation techniques that distribute risk across multiple lending platforms, collateral asset types, and geographic jurisdictions to minimise correlation risks and single points of failure. Professional portfolio managers implement systematic diversification strategies that account for platform-specific risks, regulatory environments, and operational procedures that could affect liquidation outcomes during periods of market stress or platform-specific issues.

Advanced portfolio construction methodologies utilise modern portfolio theory principles adapted for cryptocurrency lending, incorporating correlation matrices between different platforms, assets, and market conditions to optimise risk-adjusted returns while maintaining acceptable liquidation probabilities. These approaches involve continuous monitoring of cross-platform exposures, systematic rebalancing procedures, and dynamic hedging strategies that adapt to changing market conditions and platform-specific developments.

Professional risk distribution strategies include geographic diversification across different regulatory jurisdictions, platform diversification across different business models and risk management approaches, and temporal diversification that spreads borrowing activities across different market cycles and volatility regimes. These comprehensive approaches enable institutional participants to maintain substantial borrowing positions while managing liquidation risk through sophisticated risk management techniques that account for multiple sources of systematic and idiosyncratic risk.

Automated Risk Management Systems and Algorithmic Protection

Cutting-edge liquidation protection systems employ artificial intelligence and machine learning technologies that continuously monitor market conditions, position health metrics, and external risk factors to implement protective actions automatically based on predefined risk parameters and market conditions. These systems integrate with multiple data sources including price feeds, volatility indices, social sentiment analysis, and macroeconomic indicators to provide comprehensive risk assessment and automated response capabilities.

Advanced algorithmic protection systems utilise natural language processing to analyse news sentiment, social media trends, and regulatory developments that could affect cryptocurrency markets and liquidation risk. These systems implement predictive models that anticipate market movements based on multiple data sources, enabling proactive position adjustments and protective actions before traditional risk metrics indicate danger. Machine learning algorithms continuously improve their predictive accuracy by analysing historical performance and adapting to changing market dynamics.

Professional automated systems include sophisticated execution algorithms that optimise the timing and sizing of protective actions to minimise market impact and transaction costs while maximising protection effectiveness. These systems can execute complex strategies including cross-platform arbitrage for liquidation protection, automated refinancing to better terms, and dynamic hedging that adjusts protection strategies based on changing market volatility and correlation patterns that affect liquidation risk across different scenarios.

Insurance Integration and Derivative-Based Protection Strategies

Advanced liquidation protection strategies incorporate comprehensive insurance coverage and derivative-based hedging techniques that provide additional layers of protection against extreme market events and technical failures that could trigger unexpected liquidations. Professional risk managers utilise parametric insurance products, decentralised insurance protocols, and traditional insurance coverage to create comprehensive protection against various liquidation scenarios including smart contract failures, oracle manipulations, and extreme market events.

Sophisticated derivative strategies include systematic options strategies that provide downside protection for collateral assets, futures-based hedging that offsets directional market risk, and structured products that provide customised protection profiles tailored to specific risk tolerance and return objectives. These approaches require deep understanding of derivatives markets and substantial capital but can provide comprehensive protection against liquidation events while maintaining exposure to potential upside returns.

Professional insurance strategies involve comprehensive coverage assessment that evaluates different types of risks including technical risks, market risks, and operational risks that could affect liquidation outcomes. Advanced practitioners utilise multiple insurance providers, diversified coverage types, and systematic claims procedures that ensure effective protection during actual loss events. These comprehensive approaches provide multiple layers of protection that complement traditional risk management techniques and automated protection systems.

Emerging Technologies for Liquidation Protection

Artificial Intelligence and Machine Learning Applications

Cutting-edge liquidation protection systems incorporate artificial intelligence and machine learning technologies that can analyse vast amounts of market data, identify patterns that precede liquidation events, and implement protective measures proactively rather than reactively. These systems learn from historical liquidation events, market cycles, and user behavior patterns to provide increasingly sophisticated protection as they accumulate more data and experience.

Machine learning applications include predictive models that forecast liquidation probability based on market conditions, sentiment analysis that incorporates social media and news sentiment into risk assessments, and behavioral analysis that identifies unusual market patterns that may indicate impending volatility. These technologies enable more precise risk assessment and more effective timing of protective actions that can prevent liquidations before they occur.

Blockchain-Native Protection Mechanisms

Next-generation DeFi protocols are incorporating native liquidation protection mechanisms directly into their smart contract architecture, including automatic position management, built-in insurance mechanisms, and sophisticated liquidation algorithms that prioritise user protection over protocol revenue. These innovations represent a fundamental shift towards user-centric design that makes liquidation protection more accessible and effective for all participants.

Emerging blockchain technologies include cross-chain liquidation protection that can utilise assets across multiple networks for collateral management, layer-2 solutions that enable more frequent and cost-effective position adjustments, and novel consensus mechanisms that provide more predictable and stable liquidation processes. These technological advances promise to make cryptocurrency lending safer and more accessible while maintaining the decentralised and permissionless nature that makes DeFi valuable.

Conclusion

Effective liquidation protection represents the cornerstone of successful crypto borrowing strategies, requiring a comprehensive understanding of risk management principles, market dynamics, and platform-specific mechanisms that enable sustainable leveraged positions. The strategies outlined in this guide provide a systematic framework for protecting collateralised positions whilst maximising the benefits of crypto-backed lending across various market conditions and volatility scenarios.

Professional implementation of liquidation protection strategies demands continuous monitoring, proactive risk management, and strategic position adjustments that adapt to changing market conditions and evolving platform features. Success in crypto borrowing requires balancing aggressive leverage opportunities with conservative risk management practices that preserve capital and maintain long-term financial stability through systematic protection protocols.

Crypto lending platforms continue to evolve. They introduce new protection mechanisms. Automated risk management tools improve. Sophisticated monitoring systems enhance borrower safety. They maintain competitive rates. They offer flexible terms. Stay informed about platform updates. Watch regulatory changes. Learn about emerging protection technologies. This ensures you leverage the most advanced tools. Maintain secure and profitable leveraged positions.

By implementing these liquidation protection strategies, crypto borrowers can confidently navigate the lending landscape whilst minimising risks and maximising opportunities for financial growth. Successful crypto borrowing isn't about avoiding all risks. It's about understanding them. Measure them. Manage them through systematic protection strategies. Align with your financial goals. Consider your risk tolerance. Long-term success requires disciplined risk management habits. Maintain conservative collateral ratios. Continuously educate yourself about emerging technologies and market dynamics.

Professional borrowers understand liquidation protection is ongoing. It requires regular portfolio reviews. Make strategic adjustments whilst monitoring market conditions proactively and watching platform developments. As crypto lending matures, borrowers who master these strategies will capitalise on leveraged opportunities. They'll maintain financial security. They'll achieve sustainable growth.

The future of cryptocurrency lending promises even more sophisticated protection mechanisms as protocols compete to offer safer borrowing experiences. Emerging technologies including artificial intelligence-powered risk assessment, cross-chain collateral management, and decentralised insurance solutions will provide additional layers of protection for borrowers. Staying informed about these developments and adapting your protection strategies accordingly will ensure you remain at the forefront of safe and profitable crypto lending practices in the years ahead.

Sources & References

- Aave. (2025). "Aave Liquidation Mechanics". Detailed liquidation process and protection strategies.

- Compound. (2025). "Compound Liquidation Guide". Liquidation thresholds and prevention methods.

- DeFi Pulse. (2025). "Liquidation Analytics". Historical liquidation data and trends.

- CoinDesk - DeFi Liquidations Explained. Understanding liquidation mechanics and risks.

- MakerDAO - Liquidation System. Detailed documentation on collateralization and liquidation mechanisms.

Frequently Asked Questions

- How do I protect my crypto loan from liquidation?

- Use conservative LTV ratios (30-40%), set multiple price alerts, maintain emergency collateral funds equal to 20-30% of loan value, monitor HF daily, and add collateral or repay loan when approaching liquidation threshold. Never borrow at maximum LTV

- What is an HF in crypto lending?

- Health factor measures your loan safety on DeFi protocols. Above 1.0 is safe, below 1.0 triggers liquidation. Higher is safer: 2.0+ is very safe, 1.5-2.0 is moderate, 1.0-1.5 is risky. It's calculated as (Collateral Value × Liquidation Threshold) / Loan Value.

- What should I do if my HF drops below 1.5?

- Add 10-20% more collateral or repay 10-15% of your loan within 24-48 hours. Monitor your position multiple times daily. Prepare emergency funds for quick action if it drops further. Please don't wait until it reaches 1.0.

- How much emergency collateral should I keep?

- Maintain liquid reserves equal to 20-30% of your loan value in stablecoins. For a $10,000 loan, keep $2,000-3,000 ready. Store in a hot wallet on the same blockchain as your loan for instant access during emergencies.

- Can I automate liquidation protection?

- Yes, using DeFi Saver or Instadapp. Set triggers like "if HF drops below 1.8, automatically repay 10% of the loan." Costs include a 0.25% automation fee plus gas. Reduces manual monitoring but adds smart contract risk.

- What's the safest LTV ratio for crypto loans?

- Conservative ratios: Bitcoin 30-40%, Ethereum 25-35%, Altcoins 20-30%. This provides a 30-50% buffer before liquidation. Never exceed 50% LTV on volatile assets, even if platforms allow higher ratios.

- How fast can I add collateral during a crash?

- DeFi: 5-15 minutes, assuming the network is not congested. CeFi: Instant if funds are already on the platform. During crashes, network congestion can cause delays in transactions. Always keep emergency funds on the same platform/chain for the fastest response.

- What happens if I can't prevent liquidation?

- Your collateral gets sold at market price to repay the loan. You lose your collateral, plus a liquidation penalty of 5-15%. If collateral is insufficient, you may still owe the remaining debt. Learn from the experience and use more conservative ratios next time.

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.