Crypto vs Traditional Money 2025 Guide

Understand the fundamental differences between cryptocurrency and traditional fiat money. Learn the advantages and disadvantages of each system and why digital money is gaining global adoption.

Introduction

Money is changing. We are witnessing the most significant transformation since 1971, when the gold standard was abandoned. Cryptocurrency has emerged as a revolutionary alternative to traditional fiat currency systems. These government-issued currencies have dominated global finance for over half a century. This shift represents more than technological innovation. It embodies a philosophical reimagining of how value is stored, transferred, and controlled in the modern economy.

Traditional fiat money systems are controlled by central banks and governments. They have provided stability and economic coordination for decades. However, they have also introduced systemic risks. These include inflation, currency debasement, and centralised control. Such control can be subject to political manipulation and economic mismanagement. The 2008 financial crisis highlighted these vulnerabilities. Subsequent quantitative easing policies sparked renewed interest in alternative forms of money.

Cryptocurrency represents a fundamentally different approach. It utilises blockchain technology to create decentralised, programmable, and mathematically scarce digital assets. These operate independently of traditional financial institutions and government control. This innovation addresses many limitations of fiat currency. It introduces new possibilities for financial inclusion, cross-border transactions, and monetary policy. These were previously impossible or impractical to implement.

The comparison between cryptocurrency and traditional money extends beyond technical differences. It encompasses broader questions about monetary sovereignty, financial privacy, and economic stability. It also examines the role of intermediaries in financial transactions. Understanding these fundamental differences is essential. Anyone seeking to navigate the evolving financial landscape needs this knowledge. It helps make informed decisions about storing, transferring, and growing wealth in the digital age.

In 2025, the relationship between cryptocurrency and traditional money has evolved. It has moved from antagonistic competition to complementary coexistence. Central bank digital currencies (CBDCs), stablecoins, and hybrid financial products now bridge the gap. They connect traditional and digital monetary systems. This evolution has created new opportunities and challenges. Individuals, businesses, and governments must adapt to an increasingly digital financial ecosystem.

This comprehensive analysis examines the fundamental differences between cryptocurrency and traditional money. It explores their respective advantages and disadvantages. It analyses real-world use cases and adoption patterns. It provides practical guidance for understanding how these monetary systems can work together. The goal is to create a more inclusive, efficient, and resilient global financial system. This system should serve the needs of all participants in the modern economy.

The debate between cryptocurrency and traditional money is not simply about technology versus tradition. It concerns fundamentally different approaches to monetary policy, financial sovereignty, and economic participation. Traditional fiat currencies offer stability, widespread acceptance, and government backing. Cryptocurrencies provide unprecedented levels of financial autonomy, global accessibility, and programmable functionality. They can address many limitations inherent in centralised monetary systems.

Understanding these differences is crucial for navigating the evolving financial landscape of 2025 and beyond. Central bank digital currencies are emerging. Regulatory frameworks are maturing. Cryptocurrency adoption is accelerating. The lines between traditional and digital money continue to blur. This creates new opportunities and challenges. These require careful consideration and strategic planning for both individual users and institutional participants.

Problems with government currency

Traditional fiat currency (government-issued money like USD, EUR, GBP) has served us well for decades, but it comes with significant limitations that become more apparent in our digital age.

Inflation and Debasement

Central banks can print unlimited amounts of money, leading to inflation that erodes purchasing power over time. Since 1971, when the US dollar was removed from the gold standard, most major currencies have lost significant value due to monetary expansion.

Historical Examples of Currency Debasement

| Currency | Time Period | Purchasing Power Lost | Primary Cause |

|---|---|---|---|

| US Dollar | 1971-2024 | 96% | Fiat monetary system, quantitative easing |

| Turkish Lira | 2018-2023 | 85% | Political interference, monetary policy |

| Venezuelan Bolívar | 2013-2023 | 99.9% | Hyperinflation, economic mismanagement |

| Argentine Peso | 2001-2023 | 98% | Recurring economic crises, debt defaults |

The Cantillon Effect

Named after 18th-century economist Richard Cantillon, this effect describes how new money creation benefits those closest to the money printer first:

- First recipients: Banks, financial institutions, government contractors

- Early recipients: Large corporations, wealthy individuals with assets

- Late recipients: Middle class, small businesses, wage earners

- Last recipients: Fixed-income earners, savers, developing countries

This creates wealth inequality as asset prices rise before wages, benefiting asset holders at the expense of wage earners and savers.

centralised Control

Governments and central banks have complete control over monetary policy, interest rates, and money supply. This centralisation can lead to poor decisions that affect entire economies, as seen in various financial crises.

Central Bank Policy Failures

- 2008 Financial Crisis: Low interest rates fueled housing bubble

- Weimar Republic (1921-1923): Hyperinflation destroyed German economy

- Zimbabwe (2000s): Money printing led to 231 million percent inflation

- Japan (1990s-2000s): Lost decades due to monetary policy mistakes

Political Influence on Monetary Policy

Central banks, despite claims of independence, often face political pressure:

- Election cycles: Pressure to stimulate economy before elections

- Government debt: Need to keep interest rates low to service debt

- Employment targets: prioritising jobs over price stability

- International pressure: Currency wars and competitive devaluation

Banking System Inefficiencies

Operational Limitations

- Business Hours: Banks operate limited hours and close on weekends

- Geographic Restrictions: Difficult to send money across borders

- High Fees: International transfers can cost $15-50+ and take days

- Account Requirements: Need documentation, credit checks, minimum balances

- Censorship: Banks can freeze accounts or block transactions

Hidden Costs of Traditional Banking

| Service | Typical Cost | Processing Time | Hidden Fees |

|---|---|---|---|

| Domestic Wire Transfer | $15-30 | Same day | Receiving bank fees |

| International Wire | $25-50 | 1-5 days | Exchange rate markup, correspondent bank fees |

| ATM Withdrawal (Foreign) | $3-5 + 3% | Instant | Dynamic currency conversion |

| Overdraft | $35 per transaction | Instant | Multiple fees per day |

Systemic Risks in Traditional Banking

- Fractional reserve banking: Banks only hold 10% of deposits in reserve

- Bank runs: If everyone withdraws simultaneously, banks fail

- Too big to fail: Largest banks create systemic risk

- Interconnectedness: Failure of one major bank affects entire system

- Moral hazard: Government bailouts encourage risky behavior

Financial Exclusion and Inequality

According to the World Bank, approximately 1.4 billion adults worldwide remain unbanked, lacking access to basic financial services. Traditional banking systems often exclude people due to documentation requirements, geographic location, or economic status.

Barriers to Financial Inclusion

- Documentation requirements: Government ID, proof of address, employment

- Minimum balance requirements: Many can't maintain required balances

- Geographic barriers: No bank branches in rural or poor areas

- Credit history requirements: Catch-22 of needing credit to get credit

- Language barriers: Services not available in local languages

- Gender discrimination: Women face additional barriers in many countries

Global Unbanked Population by Region

| Region | Unbanked Adults | Percentage | Primary Barriers |

|---|---|---|---|

| Sub-Saharan Africa | 350 million | 57% | Distance, documentation, cost |

| South Asia | 290 million | 30% | Gender barriers, rural access |

| East Asia & Pacific | 200 million | 27% | Rural infrastructure, income |

| Latin America | 70 million | 30% | Trust, documentation |

Economic Impact of Financial Exclusion

- Reduced economic growth: Limited access to capital and credit

- Increased poverty: Inability to save, invest, or build wealth

- Higher transaction costs: Reliance on expensive informal services

- Limited business development: Entrepreneurs can't access funding

- Reduced government revenue: Cash economy harder to tax

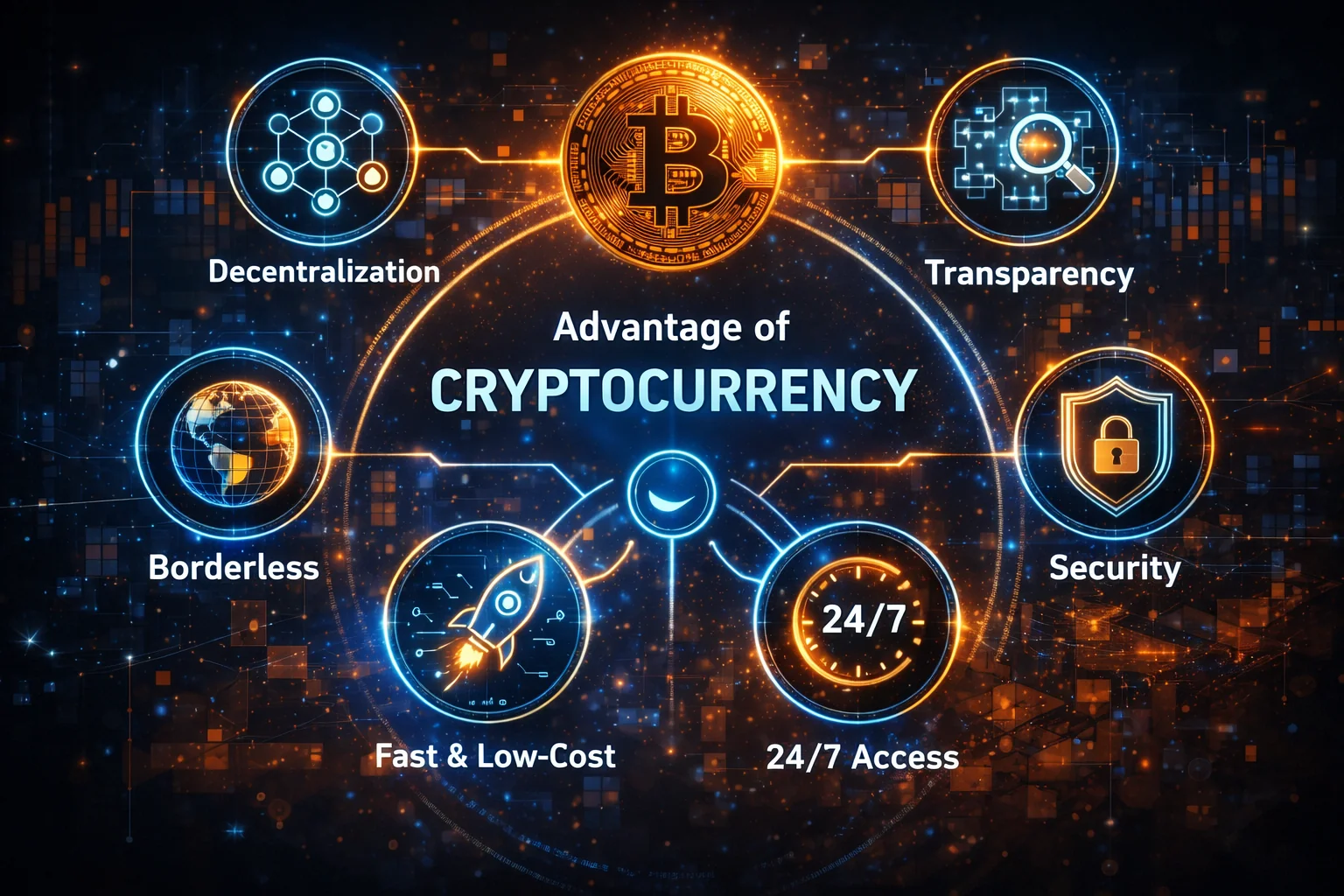

Cryptocurrency Advantages

Cryptocurrency addresses many limitations of centralised money through innovative blockchain technology and decentralised networks.

24/7 Global Access

Cryptocurrency networks operate continuously without downtime. You can send Bitcoin from New York to Tokyo at 3 AM on Christmas Day, and the transaction will be processed within minutes or hours, not days.

Network Uptime Statistics

| Network | Uptime (Since Launch) | Longest Downtime | Average Block Time |

|---|---|---|---|

| Bitcoin | 99.98% | 0 minutes | 10 minutes |

| Ethereum | 99.95% | 0 minutes | 12 seconds |

| Solana | 96.5% | 17 hours | 400ms |

| Traditional Banking | ~99.5% | Hours (maintenance) | Business hours only |

Lower Transaction Costs

International crypto transfers typically cost a few dollars regardless of the amount sent, compared to traditional wire transfers that can cost $25-50+ and take 3-5 business days.

Transaction Cost Comparison

| Transfer Method | $100 Transfer | $10,000 Transfer | Processing Time |

|---|---|---|---|

| Bitcoin | $2-5 | $2-5 | 10-60 minutes |

| Ethereum | $1-10 | $1-10 | 1-5 minutes |

| Stablecoins (Layer 2) | $0.01-0.50 | $0.01-0.50 | Seconds |

| Bank Wire Transfer | $25-50 | $25-50 | 1-5 business days |

| Western Union | $8-15 | $50-200 | Minutes to hours |

Financial Inclusion Revolution

Anyone with a smartphone and an internet connection can access cryptocurrency services. No bank account, credit check, or government documentation required - download a wallet app and you're ready to participate in the global economy.

Crypto Adoption in Developing Countries

- Nigeria: 32% of population owns cryptocurrency (highest globally)

- Vietnam: 21% adoption rate, driven by remittances

- Philippines: 20% adoption, popular for overseas worker remittances

- Turkey: 18% adoption, hedge against lira devaluation

- Peru: 16% adoption, alternative to unstable banking

Real-World Financial Inclusion Examples

- El Salvador: Bitcoin legal tender, financial inclusion for unbanked

- Kenya: M-Pesa mobile money success paved way for crypto adoption

- Venezuela: Crypto used to preserve wealth during hyperinflation

- Afghanistan: Crypto provides financial access after banking collapse

Programmable Money and Smart Contracts

Smart contracts enable money to be programmed with specific conditions and executed automatically. This opens possibilities for:

DeFi Applications

- Automated lending: Borrow against collateral without credit checks

- Yield farming: Earn interest by providing liquidity

- decentralised exchanges: Trade without intermediaries

- Synthetic assets: Create exposure to any asset

- Insurance protocols: Automated claim processing

Smart Contract Use Cases

| Application | Traditional Process | Smart Contract Process | Benefits |

|---|---|---|---|

| Insurance Claims | File claim, investigation, manual payout | Automatic payout based on data feeds | Instant, transparent, no disputes |

| Supply Chain Finance | Letters of credit, manual verification | Automatic payment on delivery confirmation | Reduced costs, faster settlement |

| Escrow Services | Third-party escrow agent | Code-based escrow conditions | Lower fees, no counterparty risk |

| Recurring Payments | Bank authorisation, manual processing | Automatic execution based on schedule | No failed payments, global access |

Transparency and Auditability

All cryptocurrency transactions are recorded on public blockchains, making the entire monetary system transparent and auditable. You can verify any transaction or check the total supply of any cryptocurrency in real-time.

Blockchain Transparency Benefits

- Real-time auditing: Anyone can verify transactions and balances

- Supply verification: Exact token supply is always known

- Transaction history: Complete record of all transfers

- Address tracking: Follow funds through the system

- Protocol governance: All changes are public and verifiable

Comparison: Crypto vs Traditional Transparency

| Aspect | Cryptocurrency | Traditional Banking |

|---|---|---|

| Transaction Visibility | All transactions public | Private, bank internal only |

| Supply Information | Real-time, exact supply | Estimated, reported periodically |

| Monetary Policy | Algorithmic, predetermined | Discretionary, behind closed doors |

| Audit Frequency | Continuous, real-time | Annual or quarterly |

Resistance to Censorship and Control

Decentralised cryptocurrencies cannot be easily censored or controlled by any single entity. This provides financial freedom in countries with authoritarian governments or unstable banking systems.

Censorship Resistance Examples

- WikiLeaks (2010): Used Bitcoin when banks blocked donations

- Canadian Truckers (2022): Bitcoin donations when banks froze accounts

- Russian sanctions (2022): Crypto used to bypass financial restrictions

- Hong Kong protests (2019): Crypto preserved financial privacy

- Nigerian protests (2020): Bitcoin used when bank accounts frozen

decentralisation Metrics

| Network | Nodes Worldwide | Mining/Validator Distribution | Censorship Resistance |

|---|---|---|---|

| Bitcoin | 15,000+ | Highly distributed | Very High |

| Ethereum | 8,000+ | Distributed staking | High |

| Traditional Banking | centralised servers | Single points of control | Low |

Detailed Comparison: Crypto vs Fiat

| Feature | Cryptocurrency | fiat currency |

|---|---|---|

| Issuance | Algorithmic, predetermined rules | Central bank discretion |

| Supply Control | Fixed or predictable inflation | Unlimited printing possible |

| Transaction Speed | Minutes to hours globally | Instant locally, days internationally |

| Transaction Costs | $0.01 - $50 depending on network | Free locally, $15-50+ internationally |

| Operating Hours | 24/7/365 | Business hours only |

| Geographic Limits | Global, internet-based | Country-specific, banking networks |

| Account Requirements | None (just need wallet) | ID, address, credit check |

| Privacy | Pseudonymous to private | Full identity required |

| Reversibility | Irreversible (generally) | Reversible (chargebacks possible) |

| Inflation Protection | Built-in scarcity (many cryptos) | Subject to monetary policy |

| Programmability | Smart contracts, DeFi | Limited automation |

| Custody | Self-custody possible | Bank custody required |

Real-World Use Case Scenarios

International Remittances

Traditional: Maria in the US wants to send $500 to her family in Mexico.

- Goes to Western Union or bank during business hours

- Pays $25-40 in fees (5-8% of transfer amount)

- Family receives money in 1-3 days

- Exchange rate markup reduces final amount

Cryptocurrency: Same scenario using Bitcoin or stablecoins.

- Sends crypto instantly from phone app

- Pays $2-5 in network fees (0.4-1% of transfer)

- Family receives money in 10-60 minutes

- Can convert to local currency at competitive rates

E-commerce Payments

Traditional: Online merchant accepting credit card payments.

- 2.9% + $0.30 per transaction in fees

- Chargeback risk for 6+ months

- Funds held for 2-7 days

- Geographic restrictions on customers

Cryptocurrency: Same merchant accepting crypto payments.

- 0.5-1% processing fees (if using payment processor)

- No chargebacks - payments are final

- Funds available immediately

- Global customer base without restrictions

Savings and Investment

Traditional: Saving money in a bank account.

- 0.01-0.5% annual interest (below inflation)

- FDIC insurance up to $250,000

- Money loses purchasing power over time

- Limited investment options

Cryptocurrency: Holding crypto or using DeFi protocols.

- Potential for higher returns (but higher risk)

- No insurance (you're responsible for security)

- Access to global DeFi yield opportunities

- 24/7 trading and liquidity options

Cryptocurrency Disadvantages

Whilst cryptocurrency offers numerous advantages, it's essential to recognise its current limitations and challenges.

Volatility

Most cryptocurrencies experience significant price volatility, making them challenging to use as stable stores of value or units of account. Bitcoin can fluctuate 10-20% in a single day, compared to major fiat currencies that typically move 1-2%.

Technical Complexity

Using cryptocurrency safely requires understanding key concepts, including private keys, seed phrases, and wallet security. Mistakes can result in permanent loss of funds with no recourse.

Regulatory Uncertainty

Cryptocurrency regulations vary significantly by country and continue to evolve. Some governments have banned crypto entirely, while others embrace it. This uncertainty affects adoption and business development.

Limited Merchant Acceptance

Whilst the cryptocurrency market is growing, its acceptance for everyday purchases remains limited compared to traditional payment methods. You can't pay for groceries with Bitcoin at most stores (yet).

Environmental Concerns

Proof-of-work cryptocurrencies, such as Bitcoin, consume significant amounts of energy, raising environmental concerns. However, newer consensus mechanisms, such as Proof of Stake, address this issue.

Irreversible Transactions

Whilst this prevents fraud, it also means mistakes cannot be undone. Send crypto to the wrong address, and it's gone forever - there's no customer service to call.

Cryptocurrency Adoption Timeline

Cryptocurrency adoption follows a predictable pattern similar to that of other revolutionary technologies, such as the internet.

Phase 1: Innovation (2009-2015)

- Bitcoin launched by tech enthusiasts

- Primarily used by developers and early adopters

- High volatility and limited real-world use

- Focus on proving the technology works

Phase 2: Early Adoption (2016-2020)

- Institutional interest begins

- Regulatory frameworks start developing

- Infrastructure improves (exchanges, wallets)

- Alternative cryptocurrencies emerge

Phase 3: Mainstream Adoption (2021-Present)

- Major corporations add Bitcoin to balance sheets

- Payment companies integrate crypto (PayPal, Visa)

- Government digital currencies (CBDCs) in development

- DeFi and NFTs bring new use cases

Phase 4: Mass Adoption (Future)

- Seamless integration with traditional finance

- Stable regulatory frameworks worldwide

- User-friendly interfaces hide complexity

- Cryptocurrency becomes as common as email

Economic Impact and Market Analysis

Global Cryptocurrency Market Statistics (2025)

| Metric | Value | Growth (YoY) | Comparison to Traditional Finance |

|---|---|---|---|

| Total Market Capitalization | $2.8 trillion | +45% | ~3% of global stock markets |

| Daily Trading Volume | $180 billion | +67% | ~15% of forex daily volume |

| Active Wallet Addresses | 420 million | +28% | ~5% of global population |

| DeFi Total Value Locked | $85 billion | +156% | ~0.1% of traditional banking assets |

| Stablecoin Market Cap | $180 billion | +89% | Larger than many national currencies |

Institutional Adoption Trends

Corporate Treasury Holdings

| Company | Bitcoin Holdings | Value (USD) | % of Treasury |

|---|---|---|---|

| MicroStrategy | 174,530 BTC | $8.7 billion | ~90% |

| Tesla | 9,720 BTC | $485 million | ~2% |

| Block (Square) | 8,027 BTC | $400 million | ~5% |

| Marathon Digital | 15,741 BTC | $785 million | ~75% |

Financial Services Integration

- Payment Processors: PayPal, Visa, Mastercard offer crypto services

- Investment Banks: Goldman Sachs, JPMorgan provide crypto trading

- Asset Managers: BlackRock, Fidelity launch Bitcoin ETFs

- Insurance Companies: MassMutual, New York Life hold Bitcoin

- Pension Funds: Several state pension funds allocate to crypto

Macroeconomic Benefits of Cryptocurrency

Financial Inclusion Impact

- Remittance Cost Reduction: Average fees dropped from 7% to 2-3% with crypto

- Banking the Unbanked: 180 million new people gained financial access

- Cross-Border Trade: $45 billion in international trade settled via crypto

- Micropayments: Enabled new business models for content creators

Innovation and Job Creation

| Sector | Jobs Created | Investment (2025) | Key Innovations |

|---|---|---|---|

| Blockchain Development | 285,000 | $12 billion | Smart contracts, Layer 2 solutions |

| DeFi Protocols | 45,000 | $8 billion | Automated market makers, yield farming |

| Crypto Mining | 120,000 | $15 billion | Renewable energy integration |

| Crypto Exchanges | 95,000 | $6 billion | Institutional custody, compliance |

Global Regulatory Landscape 2025

Regional Regulatory Approaches

Progressive Jurisdictions

- European Union: MiCA regulation provides comprehensive framework

- Singapore: Clear guidelines for crypto businesses and DeFi

- Switzerland: Crypto-friendly banking and regulatory environment

- United Arab Emirates: Dubai becomes global crypto hub

- El Salvador: Bitcoin legal tender, government adoption

Restrictive Jurisdictions

- China: Complete ban on crypto trading and mining

- India: High taxation and regulatory uncertainty

- Russia: Limited legal framework, sanctions complications

- Turkey: Payment restrictions but mining allowed

Evolving Frameworks

- United States: State-by-state approach, federal clarity pending

- United Kingdom: Developing comprehensive crypto regulation

- Japan: Established framework expanding to include DeFi

- Canada: Provincial licensing with federal oversight

Central Bank Digital Currencies (CBDCs)

| Country | CBDC Status | Launch Timeline | Key Features |

|---|---|---|---|

| China | Live (Digital Yuan) | 2020-2025 rollout | Programmable money, offline payments |

| European Union | Development | 2026-2028 | Privacy-focused, interoperable |

| United States | Research | 2027-2030 | Federal Reserve exploring options |

| United Kingdom | Pilot | 2025-2027 | Digital pound trials |

| Nigeria | Live (eNaira) | 2021 launch | Financial inclusion focus |

The Future: Coexistence, Not Replacement

Rather than completely replacing fiat currency, cryptocurrency is more likely to coexist and complement existing financial systems, each serving different needs and use cases.

conventional money Will Remain For:

- Everyday local purchases

- Stable value storage (low volatility)

- Government services and taxes

- Regulated financial products

- Consumer protection scenarios

Cryptocurrency Will Excel For:

- International transfers and remittances

- Programmable money and smart contracts

- Financial inclusion for the unbanked

- Hedge against inflation and debasement

- Innovation in financial services (DeFi)

Central Bank Digital Currencies (CBDCs)

Many countries are developing digital versions of their national currencies that combine the benefits of both systems:

- Digital convenience of cryptocurrency

- Stability and backing of government currency

- Programmable features for policy implementation

- Maintained government control and regulation

Start Your Crypto Journey

Ready to experience cryptocurrency advantages? Start with these trusted platforms:

- Binance - World's Largest Exchange - Best for beginners with low fees

- Coinbase - US Regulated Platform - Most user-friendly for Americans

- Ledger Hardware Wallet Review - Secure offline storage

Advanced Monetary Systems and Professional Financial Analysis

Institutional Monetary Policy and Central Bank Digital Currencies

Professional understanding of monetary systems requires comprehensive analysis of central bank digital currencies (CBDCs), institutional monetary policy frameworks, and sophisticated financial infrastructure that shapes the evolution of both traditional and cryptocurrency systems. Institutional monetary analysis incorporates advanced economic theory, comprehensive policy assessment, and sophisticated market dynamics that influence monetary system development whilstcreating opportunities and challenges for both traditional finance and cryptocurrency adoption through professional monetary analysis and institutional financial expertise designed for advanced economic understanding.

Central bank digital currencies (CBDCs) are being developed worldwide. These digital currencies combine traditional monetary policy with blockchain technology. They enable digital currency functionality whilst maintaining financial stability. Professional monetary policy analysis requires understanding economic theory and statistical techniques. This enables informed assessment of monetary system evolution. It helps manage economic risks and opportunities through professional analysis.

Quantitative Financial Analysis and Mathematical Monetary Models

Advanced monetary system analysis uses sophisticated quantitative models. These include economic forecasting, risk assessment, and mathematical optimisation. They enable informed financial decisions whilst managing portfolio risks. Quantitative monetary analysis incorporates econometric techniques and correlation modelling. It includes comprehensive backtesting frameworks. These enable systematic monetary system evaluation whilst maintaining appropriate risk management.

Mathematical monetary models implement advanced algorithms for economic forecasting. They provide sophisticated risk measurement and performance attribution. This maximises financial system understanding whilst maintaining analytical rigour. Professional practitioners use advanced statistical techniques and scenario analysis. They employ sophisticated optimisation methods. These enable continuous improvement in monetary analysis whilst managing economic volatility.

Technology Integration and Financial Innovation

Modern monetary systems require comprehensive knowledge of financial technology evolution. This includes advanced payment systems and sophisticated digital infrastructure. Technology integration includes blockchain development and digital payment creation. It provides comprehensive financial infrastructure. This enables advanced monetary utilisation whilst maintaining security and operational efficiency.

Financial innovation implements advanced scalability solutions. It includes sophisticated interoperability protocols and comprehensive security enhancements. These improve monetary system functionality whilst maintaining stability principles. Professional technology development requires advanced programming knowledge. It needs comprehensive security assessment and sophisticated operational controls. These enable financial innovation whilst maintaining performance and user experience.

Monetary Policy Implications and Economic Impact

Cryptocurrency adoption creates significant implications for traditional monetary policy. Central banks must adapt their approaches whilst maintaining economic stability. Professional monetary policy analysis includes understanding cryptocurrency market dynamics. It requires implementation of comprehensive regulatory frameworks. Adaptive policy mechanisms address digital currency challenges whilst maintaining macroeconomic stability.

Economic impact assessment evaluates the effects of cryptocurrencies on inflation, monetary velocity, and financial stability. This requires sophisticated analytical frameworks and comprehensive monitoring systems. These enable informed policy decisions whilst maintaining economic equilibrium. Professional economic analysis includes systematic evaluation of digital currency adoption patterns. It implements comprehensive impact measurement systems. Adaptive policy responses address emerging challenges whilst maintaining economic stability.

Future monetary system evolution includes integrating digital currencies with traditional financial infrastructure. This involves developing central bank digital currencies (CBDCs). It creates hybrid monetary frameworks that combine cryptocurrency innovation with traditional stability mechanisms. Professional monetary system development requires understanding complex economic relationships. It implements sophisticated policy coordination mechanisms. Comprehensive regulatory frameworks enable monetary innovation whilst maintaining economic stability.

Adoption Challenges and Market Integration

Cryptocurrency adoption faces significant challenges. These include regulatory uncertainty, technological complexity, and market volatility. Comprehensive solutions and systematic approaches are required. These enable mainstream integration whilst maintaining innovation. Professional adoption strategies include development of user-friendly interfaces. They implement comprehensive educational programmes. Sophisticated risk management frameworks address adoption barriers whilst maintaining cryptocurrency advantages.

Market integration requires understanding traditional financial system constraints. It needs implementation of sophisticated interoperability solutions. Comprehensive regulatory compliance frameworks enable seamless cryptocurrency adoption. These maintain stability of existing financial infrastructure. Professional integration strategies encompass systematic evaluation of market requirements. They implement adaptive technology solutions. Comprehensive stakeholder engagement programmes facilitate cryptocurrency adoption whilst addressing traditional finance concerns.

Future adoption success depends on continued technological innovation. Regulatory clarity development is essential. Comprehensive market education addresses adoption barriers whilst maintaining cryptocurrency innovation. Professional adoption management includes systematic evaluation of market dynamics. It implements adaptive adoption strategies. Comprehensive ecosystem support enables sustainable cryptocurrency growth whilst maintaining market stability and user confidence.

Technological Innovation and Future Development

Cryptocurrency technological innovation encompasses advanced blockchain development. It includes sophisticated consensus mechanisms and comprehensive scalability solutions. These address current limitations whilst maintaining security and decentralisation principles. Professional technology development implements layer-2 scaling solutions. It includes advanced interoperability protocols and sophisticated privacy enhancements. These improve cryptocurrency functionality whilst maintaining operational efficiency and user experience.

Future cryptocurrency development includes evolution of quantum-resistant cryptography. It integrates advanced artificial intelligence. Sophisticated cross-chain communication protocols enable seamless blockchain interoperability. These maintain security and decentralisation principles. Professional cryptocurrency innovation requires understanding emerging technologies. It implements forward-thinking development strategies. Comprehensive innovation frameworks capitalise on technological advances whilst maintaining practical application focus.

Strategic technological positioning requires continuous monitoring of emerging innovations. Systematic evaluation of development opportunities is essential. Implementation of adaptive strategies capitalises on technological advances. These maintain competitive advantages and operational excellence. Professional cryptocurrency development includes systematic evaluation of emerging technologies. It implements experimental development approaches. Comprehensive testing frameworks ensure reliable innovation whilst maintaining security and operational excellence.

Economic Transformation and Global Impact

Cryptocurrency-driven economic transformation encompasses fundamental changes to global financial systems. It implements decentralised economic models. Innovative value transfer mechanisms challenge traditional monetary paradigms. These create new opportunities for economic participation and financial inclusion. Professional economic analysis includes systematic evaluation of cryptocurrency impact. It implements comprehensive market assessment frameworks. Adaptive economic models account for digital currency integration whilst maintaining economic stability.

Global economic impact includes transformation of international trade. Programmable money systems are being implemented. Sophisticated cross-border payment solutions reduce transaction costs. These improve settlement efficiency and financial accessibility. Professional global economic management requires understanding complex international monetary relationships. It implements sophisticated policy coordination mechanisms. Comprehensive regulatory frameworks enable cryptocurrency integration whilst maintaining international economic stability.

Economic paradigm shifts encompass evolution from centralised monetary control to decentralised financial systems. Algorithmic monetary policies are being implemented. Community-governed economic frameworks enable democratic participation in monetary decision-making. These maintain economic stability and growth objectives. Professional economic transformation management includes systematic evaluation of paradigm shift implications. It implements adaptive economic strategies. Comprehensive transition frameworks enable successful economic evolution whilst maintaining stability and prosperity.

Financial Inclusion and Accessibility Revolution

Cryptocurrency enables unprecedented financial inclusion. It provides banking services to unbanked populations. Permissionless financial systems are being implemented. Accessible investment opportunities transcend traditional geographic and economic barriers. These maintain security and operational efficiency. Professional financial inclusion strategies include development of user-friendly cryptocurrency interfaces. Comprehensive educational programmes are implemented. Sophisticated support systems enable global financial participation whilst addressing accessibility challenges.

The accessibility revolution encompasses development of mobile-first cryptocurrency solutions. Simplified user interfaces are being implemented. Comprehensive financial literacy programmes enable widespread cryptocurrency adoption. These maintain security and operational reliability. Professional accessibility management requires understanding diverse user needs. Inclusive design principles are implemented. Comprehensive support frameworks address barriers to cryptocurrency adoption whilst maintaining functionality and security.

Global financial empowerment includes implementation of microfinance solutions. Decentralised lending platforms are being developed. Innovative savings mechanisms provide financial services to underserved populations. These maintain competitive rates and operational efficiency. Professional empowerment strategies encompass systematic evaluation of underserved market needs. Tailored cryptocurrency solutions are implemented. Comprehensive support systems enable financial independence whilst maintaining security and regulatory compliance.

Cross-Border Payment Innovation

Cryptocurrency revolutionises cross-border payments through instant settlement systems. Traditional correspondent banking delays are eliminated. Cost-effective international transfer mechanisms reduce remittance costs. These improve transaction speed and reliability. Professional cross-border payment management includes development of sophisticated routing algorithms. Comprehensive compliance frameworks are implemented. User-friendly international transfer interfaces enable seamless global money movement whilst maintaining regulatory adherence.

Institutional Adoption and Corporate Integration

Institutional cryptocurrency adoption encompasses corporate treasury management. Blockchain-based business processes are being implemented. Sophisticated cryptocurrency investment strategies enable professional-grade digital asset management. These maintain fiduciary responsibilities and regulatory compliance. Professional institutional adoption includes systematic evaluation of cryptocurrency integration opportunities. Comprehensive risk management frameworks are implemented. Sophisticated operational procedures ensure successful institutional cryptocurrency participation whilst maintaining operational excellence.

Corporate integration strategies include implementation of cryptocurrency payment systems. Blockchain-based supply chain solutions are being developed. Innovative customer engagement programmes leverage cryptocurrency capabilities. These maintain operational efficiency and customer satisfaction. Professional corporate cryptocurrency management requires understanding complex business requirements. Sophisticated compliance frameworks are implemented. Comprehensive integration strategies enable successful cryptocurrency adoption whilst maintaining business objectives.

Enterprise Blockchain Solutions

Enterprise blockchain implementation encompasses development of private blockchain networks. Sophisticated smart contract systems are being implemented. Comprehensive data management solutions enable business process optimisation. These maintain security and operational reliability. Professional enterprise blockchain management includes systematic evaluation of blockchain applications. Comprehensive security frameworks are implemented. Sophisticated integration strategies enable successful enterprise blockchain adoption whilst maintaining business continuity.

Regulatory Compliance and Risk Management

Professional institutional cryptocurrency operations require comprehensive regulatory compliance frameworks. Sophisticated risk management systems are essential. Advanced monitoring capabilities ensure regulatory adherence whilst maintaining operational efficiency. Institutional compliance management includes systematic evaluation of regulatory requirements. Comprehensive reporting systems are implemented. Proactive compliance strategies address regulatory changes whilst maintaining institutional cryptocurrency effectiveness.

Environmental Sustainability and Green Finance

Cryptocurrency environmental sustainability encompasses development of energy-efficient consensus mechanisms. Renewable energy mining operations are being implemented. Carbon-neutral blockchain networks address environmental concerns. These maintain security and operational efficiency. Professional sustainability management includes systematic evaluation of environmental impact. Comprehensive carbon offset programmes are implemented. Sophisticated green technology solutions enable sustainable cryptocurrency operations whilst maintaining performance and security.

Green finance innovation includes development of environmental impact tokens. Carbon credit trading systems are being implemented. Sustainable investment mechanisms enable environmental funding. These maintain financial returns and operational efficiency. Professional green finance management requires understanding environmental finance principles. Sophisticated impact measurement systems are implemented. Comprehensive sustainability frameworks enable effective environmental financing whilst maintaining investment performance.

Sustainable Mining and Validation

Sustainable cryptocurrency mining encompasses implementation of renewable energy systems. Energy-efficient mining hardware is being developed. Comprehensive environmental monitoring frameworks minimise environmental impact. These maintain network security and operational reliability. Professional sustainable mining management includes systematic evaluation of energy sources. Comprehensive efficiency optimisation programmes are implemented. Sophisticated environmental compliance procedures ensure sustainable mining operations whilst maintaining profitability.

Climate Action and Carbon Markets

Cryptocurrency enables innovative climate action through transparent carbon credit systems. Automated environmental compliance mechanisms are being implemented. Sophisticated climate finance solutions enable effective environmental funding. These maintain transparency and operational efficiency. Professional climate action management includes systematic evaluation of environmental projects. Comprehensive impact verification systems are implemented. Sophisticated funding mechanisms enable effective climate action whilst maintaining accountability and performance.

Digital Identity and Privacy Revolution

Cryptocurrency enables revolutionary digital identity solutions. Self-sovereign identity systems are being implemented. Privacy-preserving authentication mechanisms are being developed. Decentralised identity management platforms provide users with complete control over personal data. These maintain security and operational efficiency. Professional digital identity management includes systematic evaluation of privacy requirements. Comprehensive security frameworks are implemented. Sophisticated identity verification systems enable secure digital interactions whilst maintaining user privacy and autonomy.

The privacy revolution encompasses development of zero-knowledge proof systems. Advanced cryptographic privacy techniques are being implemented. Comprehensive anonymity frameworks enable private financial transactions. These maintain regulatory compliance and operational transparency where required. Professional privacy management requires understanding complex cryptographic principles. Sophisticated privacy-preserving technologies are implemented. Comprehensive privacy frameworks enable effective privacy protection whilst maintaining functionality and compliance.

Decentralised Governance and Democracy

Cryptocurrency enables innovative governance models through decentralised autonomous organisations (DAOs). Transparent voting systems are being developed. Community-driven decision-making frameworks enable democratic participation in organisational governance. These maintain operational efficiency and accountability. Professional decentralised governance management includes systematic evaluation of governance requirements. Comprehensive voting mechanisms are implemented. Sophisticated consensus systems enable effective community governance whilst maintaining organisational objectives.

Programmable Money and Smart Contracts

Programmable money revolutionises financial automation through sophisticated smart contract systems. Automated payment mechanisms are being developed. Comprehensive financial automation frameworks enable complex financial operations. These maintain security and operational reliability. Professional programmable money management includes systematic evaluation of automation opportunities. Comprehensive smart contract security frameworks are implemented. Sophisticated financial automation systems enable effective financial programming whilst maintaining security and performance.

Conclusion

The comparison between cryptocurrency and traditional money reveals a complex evolution. This is not a simple choice between old and new. Instead, we are moving towards a more diverse and inclusive financial ecosystem. Both systems offer distinct advantages. Both face unique challenges. Their coexistence is likely to define the future of global finance. Neither system will dominate alone.

Traditional fiat currencies provide stability, widespread acceptance, and regulatory backing. These qualities make them suitable for everyday transactions and long-term financial planning. Their integration with existing economic systems ensures they will remain central to global commerce. Government backing and established infrastructure support this position. However, they have limitations. These include inflation risk, centralised control, and barriers to financial inclusion. These limitations create opportunities for alternative monetary systems.

The Path forwards

Cryptocurrency addresses many of these limitations. It does this through decentralisation, programmability, and global accessibility. It offers unprecedented financial sovereignty and innovation potential. Yet it faces challenges. These include volatility, technical complexity, and regulatory uncertainty. These must be addressed for mainstream adoption. The most promising future lies not in replacement but in complementary coexistence. Each system should serve its optimal use cases.

Central bank digital currencies represent a bridge between these worlds. They combine the stability and backing of traditional money with the technological advantages of digital assets. As these systems mature and integrate, users will benefit. They will gain increased choice, improved functionality, and enhanced financial inclusion across the global economy.

Making Informed Decisions

Individuals and institutions must navigate this evolving landscape. The key is understanding the strengths and limitations of each system. Use them strategically based on specific needs and circumstances. Traditional money remains optimal for stability and everyday transactions. Cryptocurrency excels in cross-border transfers, financial innovation, and situations requiring censorship resistance or rapid settlement.

As we move through 2025 and beyond, the financial system will likely become increasingly hybrid. Traditional and digital money will work together. This will create a more efficient, inclusive, and resilient global economy. Success in this environment requires staying informed. You must understand developments in both systems. Maintain flexibility to adapt to changing circumstances and opportunities.

The integration of artificial intelligence and machine learning is accelerating innovation. This applies to both traditional banking and cryptocurrency platforms. User experiences are improving. Smart contracts and programmable money features are enabling new financial products. These were impossible with traditional systems alone. Meanwhile, traditional financial institutions are adopting blockchain technology. They are improving settlement times and reducing costs. This creates a convergence that benefits all users.

Sources & References

This article is based on research from reputable cryptocurrency and financial sources. All information is current as of the publication date and subject to change as the cryptocurrency market evolves.

Frequently Asked Questions

- Is cryptocurrency better than centralised money?

- Neither is universally better - they serve different purposes. Cryptocurrency excels for international transfers, financial inclusion, and programmable money, while traditional money offers stability and widespread acceptance for daily transactions.

- Why do cryptocurrencies fluctuate in price so much?

- Cryptocurrency markets are still relatively small and immature compared to traditional currency markets. Limited liquidity, speculation, regulatory news, and adoption developments all contribute to significant price volatility.

- Can governments ban cryptocurrency?

- Governments can restrict or ban cryptocurrency exchanges and businesses within their borders, but they cannot completely shut down decentralised networks like Bitcoin due to their global, peer-to-peer nature.

- Will cryptocurrency replace traditional money completely?

- Unlikely. Coexistence is more probable, with each system serving different needs: crypto for global transfers and programmable money, and traditional currency for local transactions and stability.

- How do I protect myself from cryptocurrency scams?

- Never share private keys, verify all website URLs, avoid "get rich quick" schemes, use reputable exchanges, and remember that legitimate projects never ask for your crypto or promise guaranteed returns.

- What happens if I lose my cryptocurrency wallet?

- If you lose access to your wallet and don't have backup seed phrases, your cryptocurrency is permanently lost. This is why proper backup and security practices are essential.

- How do Central Bank Digital Currencies (CBDCs) compare to cryptocurrencies?

- CBDCs are digital versions of government currencies that combine digital convenience with government backing and control. Unlike decentralised cryptocurrencies, CBDCs are centrally controlled and may include programmable features to implement policy.

- What is the environmental impact of cryptocurrency?

- Bitcoin mining consumes significant energy, but newer cryptocurrencies use energy-efficient consensus mechanisms like Proof of Stake. The industry is increasingly focused on renewable energy and carbon-neutral operations.

- How do transaction fees compare between crypto and traditional payments?

- Crypto fees vary by network: Bitcoin ($2-5), Ethereum ($1-10), Layer 2 solutions ($0.01-0.50). Traditional international wires cost $25-50+. For small amounts, traditional payments may be more cost-effective; for large international transfers, cryptocurrency is typically more cost-effective.

- Can cryptocurrency help during economic crises?

- Cryptocurrency can provide financial access when traditional banking fails, preserve wealth during hyperinflation, and enable cross-border transactions during capital controls. However, it's also volatile and requires technical knowledge to use safely.

- What role do stablecoins play in the crypto vs fiat debate?

- Stablecoins bridge crypto and traditional finance by maintaining stable value while offering crypto benefits like 24/7 transfers and programmability. They're increasingly used for international trade and as a store of value in unstable economies.

← Back to Cryptocurrency Guide 2025

← Back to Crypto Investing Blog Index

Financial Disclaimer

This content is not financial advice. All information provided is for educational purposes only. Cryptocurrency investments carry significant investment risk, and past performance does not guarantee future results. Always do your own research and consult a qualified financial advisor before making investment decisions.